How equity loans can harm homeowners

To a homeowner who needs some extra money, an equity loan may seem like a good idea.

However, the loan, which uses the equity of the home as collateral, can very easily backfire. Philadelphia Realtor® Al Perry, who has been in the real estate business for more than two decades, recently saw a family lose a home that had been theirs for generations.

Perry had an investor client who purchased a home that was in foreclosure in the Wynnfield area of Philadelphia. The investor paid only $235,000, and Perry said the home needs significant work, but it will be a “showpiece” once its done.

Interested in the history of the home, Perry began reading about the mortgage and sale of house.

“It had been in the same family for 77 years,” Perry said. “The private owner before our current client inherited the home with no mortgage. In 1996, she refinanced the home for $100,000 and what followed over the next 15 years was 10 additional equity loans or refinances, culminating with a $562,500 mortgage in 2011.”

The loan, a modified FHA mortgage, was originally for $397,000, but was restructured to the much higher balance to capture deferred interest. To keep the payments lower and more “affordable,” the mortgage term was also adjusted to 61 years. With such a long term, each on time payment would barely pay off any principal balance. It’s like removing all the sand from the beach one bucket at a time. Clearly, the payments were not affordable enough because the bank eventually foreclosed on the home in 2018.

“I don’t pretend to know the financial circumstances that the owner may have faced over the years,” said Perry. “Sometimes, people have good reasons for tapping into a property’s equity. What I can tell you is the only significant upgrade to the property that was done over that period was a massive in-ground pool that now will likely be filled in because of neglectful maintenance.”

“It’s such a tragic story,” added Perry. “A family builds equity over many years and hands a property free and clear of a mortgage to a family heir, who then subsequently slowly digs themselves into a $562,500 financial hole. The saddest part to me is likely the last eight years where they found a way to barely keep their heads above water before drowning in debt and losing their property to the bank. Likely, this was the complete opposite wish of the mother or father who left family the home as part of their estate years earlier.”

Perry said Realtors® can help encourage clients to think before taking out an equity loan, and to talk to a financial advisor before taking such steps.

“Never assume your home’s value will continue to rise,” he said. “This is a sucker’s bet and one that can leave you with no equity or even worse, ‘upside down’ equity, where you owe more than the home is worth for years.”

Perry is now an advocate for 15-year mortgages. “There is significantly less interest paid on a 15-year loan,” he said. While Realtors® are not primarily in the mortgage business, encourage your clients to reach out to you if they’re looking to take out an equity loan. If you’re not comfortable giving advice, you can point them in the direction of the right person.

“This situation tugged at my heart strings,” added Perry.

Topics

Share this post

Member Discussion

Recent Articles

-

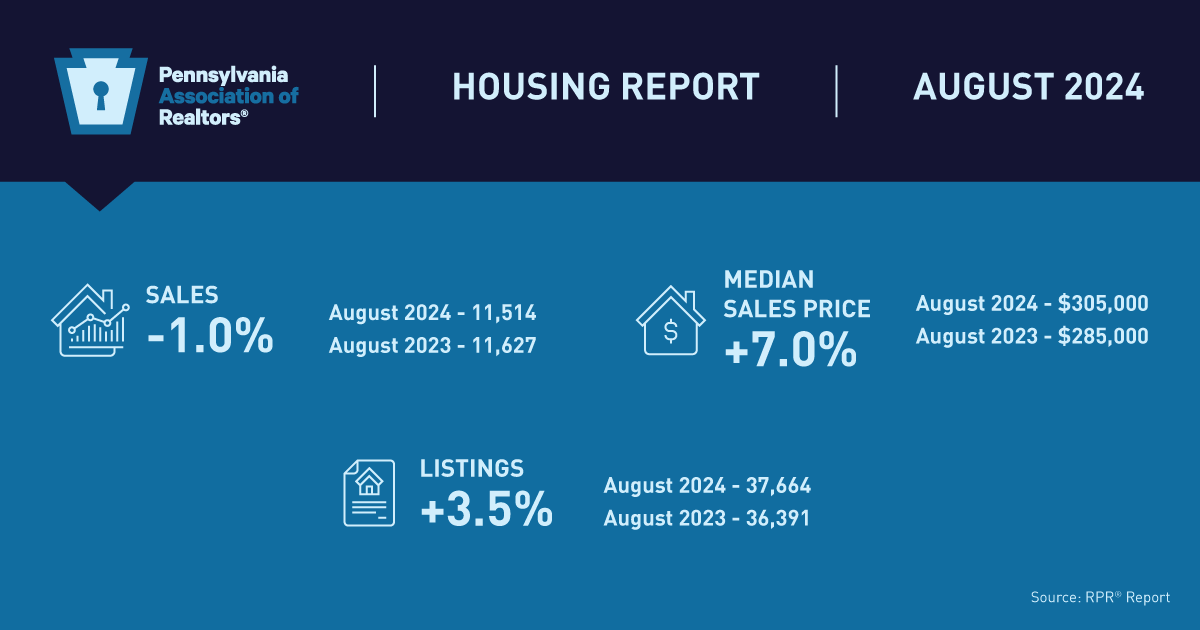

Pennsylvania Median Home Sales Price Holds Steady in August

- September 20, 2024

- 2 min. read

According to PAR’s housing report, the median home sales price remained about the same as July, at $305,000 last month.

-

PAR Honors Three Dedicated Realtors®

- September 19, 2024

- 4 min. read

Sherrie Miller received the Lifetime Achievement Award, Helen Miernicki received the Realtor® of the Year Award and Glenn Yoder received the Realtor® Active in Politics Award.

-

More Seniors Struggle Financially, Consider Roommates

- September 18, 2024

- 2 min. read

Struggling with high levels of debt and expensive housing costs, many seniors are becoming more receptive to living with roommates.

Daily Emails

You’ll be the first to know about real estate trends and various legal happenings. Stay up-to-date by subscribing to JustListed.